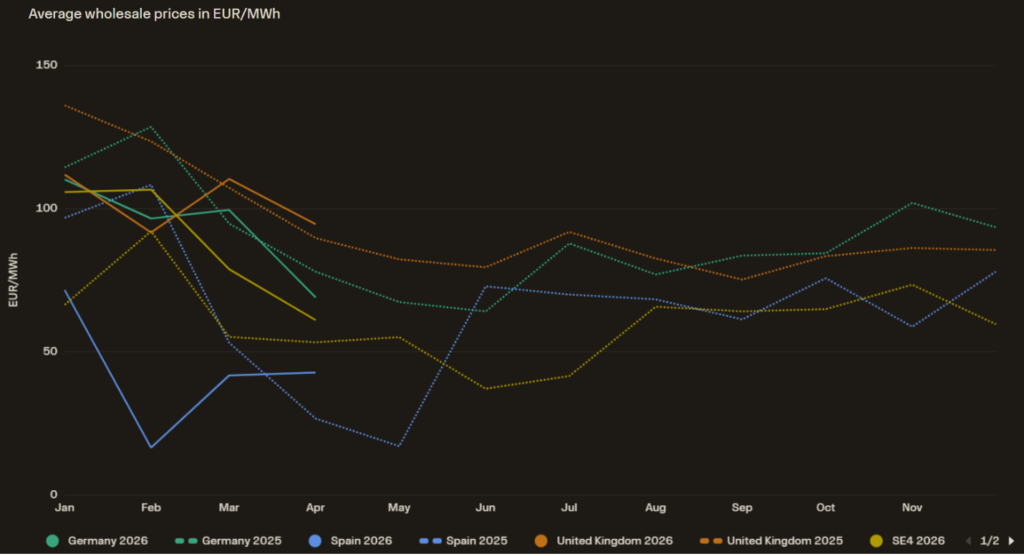

Wholesale power prices across Europe remained broadly stable or slightly lower in April, supported by strong renewable generation, particularly solar. The Nordics eased from March highs due to improved hydrology and stronger wind output, while Iberia and France continued to record very low prices during periods of strong solar generation. Solar capture rates decreased significantly while capture rates for wind remained more stable. Negative and zero-price hours increased across several markets as renewable penetration continued to rise, while elevated gas prices and geopolitical tensions continued to support prices in more gas-dependent regions.

The Veyt PPA price index remained volatile throughout April, moving largely in line with commodity and power futures markets amidst continued geopolitical tensions. Prices fluctuated during the month but stayed below the peaks seen in late March 2026. In the Nordics, hydrological constraints continued to support elevated pricing levels. In the UK, bullish carbon prices due to potential linking with the EU ETS translated into higher PPA prices towards end of the month.

As market volatility increases, reliable PPA valuations are more important than ever. Request your free PPA benchmark from Veyt today.

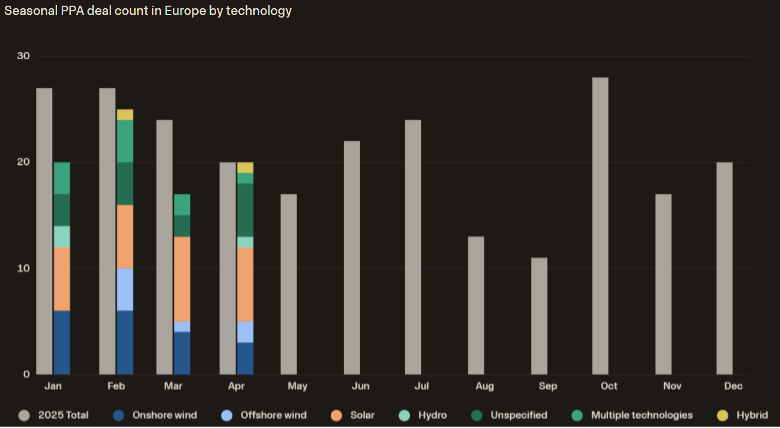

April 2026 continued the trend of relatively low contracted capacity despite strong deal activity and high contracted volumes. Twenty deals were announced during the month, matching activity levels seen in recent month, while contracted volumes increased significantly compared to March. Large transactions in the Nordics and under Italy’s Energy Release 2.0 scheme were key drivers of market activity.

The UK and Poland were the most active markets, each recording three deals, followed by Germany, Ireland, Italy and Norway with two deals each. Activity was geographically diverse, with additional agreements signed in France and Greece.

Solar PV remained the dominant technology with seven announced agreements, followed by onshore and offshore wind. The month also saw continued growth in hybrid and multi-technology structures, alongside several large portfolio-style agreements where specific technologies were not disclosed.

Overall, the market continues to demonstrate resilience despite ongoing geopolitical uncertainty and commodity price volatility. Strong deal flow and increased transaction diversity suggest that corporate demand for long-term renewable procurement remains solid across Europe.

France’s Ministry of Defence signed a landmark 30-year solar PPA with Axpo linked to a 42 MWp solar PV project on a former military site.

Enfinity Global and Acciona Energía signed major agreements under Italy’s Energy Release 2.0 scheme, adding to a total of 4.1 TWh contracted under the scheme so far this year.

Hydro Energi and Statkraft signed two long-term PPAs in Norway covering 12.3 TWh over ten years for Hydro’s aluminium operations.

PPAs from portfolios of renewable generation across bidding zones are gaining interest, as they offer diversified generation profiles, reduce imbalance exposure and mitigate risk. In a recent client case, Veyt quantified potential portfolio gains for a client in the Nordics.

PPA deal count in Europe

Average power price for selected markets

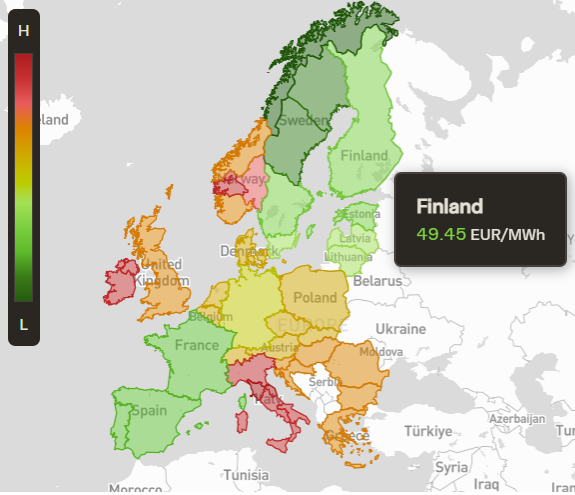

Average power price across Europe April 2026

Veyt provides consistent price benchmarks, transaction data, underlying datasets, and asset-level valuation tools through its PPA Intelligence platform. This enables you to track market movements, benchmark prices across transactions, and run your own valuations based on specific location, profile, and contract terms.

For more complex cases, including hybrid PPAs for co-located BESS, portfolios of multiple technologies or non-standard contract structures, Veyt also delivers sensitivity analyses and independent price benchmarks to support negotiations.