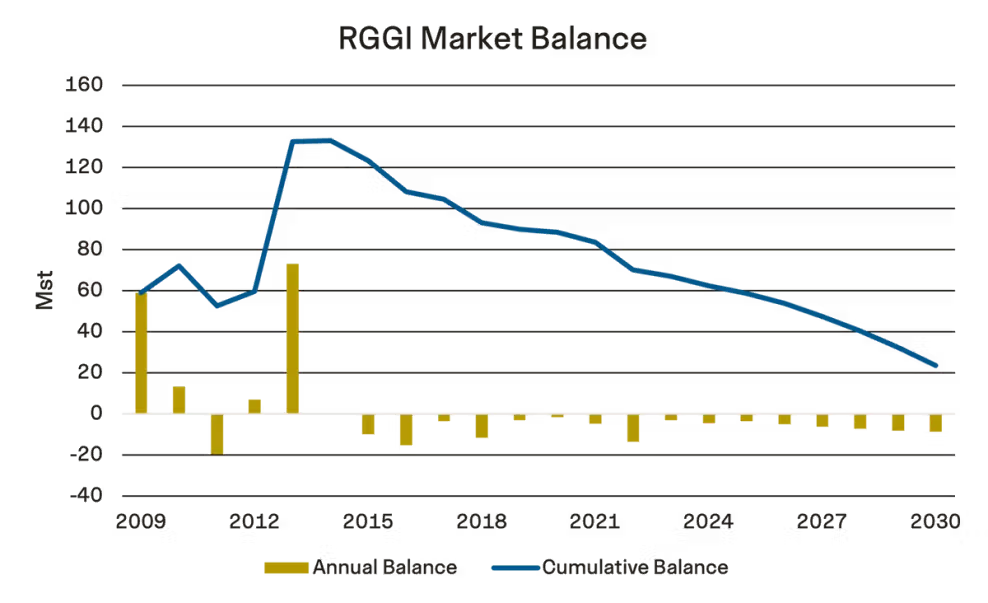

Veyt expects that the reduction in cumulative supply over the next several years will lead to a significant increase in allowance prices at both auctions and on the secondary market. The RGGI benchmark contract has already seen a 70% increase since the start of the year – reaching a record-high USD 27.85/st settlement on 20 August.

The price increase has been driven primarily by high demand and anticipation of the program reforms. As current spikes in price are due to regulatory anticipation and uncertainty, the contract is likely to see a significant correction once RGGI regulators provide final updates from the review process, like by the beginning of 2025 in order for a 2026 implementation, and could potentially push contract prices down to levels near USD 20.00/st.

“RGGI is accelerating member states decarbonization plans by reducing allowance supply, helping them lead the way in both the US and globally. Higher demand sets the stage for a bullish market with increased prices and new renewable investment. For RGGI states, this means being ahead of the game –with a green grid from 2040, states will be able to source their increasing EV power demand with clean electricity, making to a more well-rounded sustainability transition.” says Luke Sideropoulos, North America carbon analyst.

For further details on the RGGI supply and demand forecast, click here.

While a short-term bearish correction seems likely, the RGGI benchmark contract is nevertheless expected to see a long-term bullish price trend. Utilities have a fourteen-year adjustment window from 2026 to 2040 before supply falls to zero. Veyt expects abatement costs to be high in the first half of this period, and therefore expect strong demand for allowances during those years. Achieving renewable targets throughout the region, particularly offshore wind, by 2035 will play a key role in mitigating accumulating demand and major spikes in price in subsequent years.

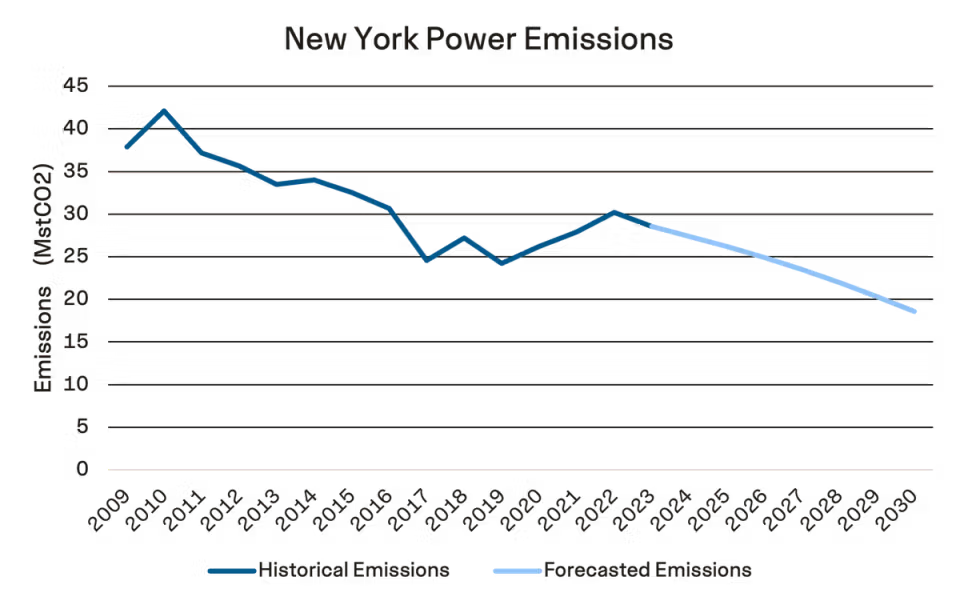

According to Veyt’s modelling, a reduction of approximately 21 million in regional power emissions is envisioned from 2024 to 2030. Almost every state in RGGI will see net reductions in their power emissions by the end of the decade, with many states relying on existing nuclear generation as a means of easing their transition to renewable energy sources (primarily solar and wind). The largest reduction in emissions will come from New York, which is forecasted to see about 33% reduction from 2023 emissions by 2030. Other notable reductions will come from Connecticut, Maryland, and New Jersey that are forecasted to see net reductions of about 5 Mst, 4 Mst, and 2 Mst by 2030 respectively.