Europe’s economy is required to become climate-neutral by 2050 by law. That means achieving net zero greenhouse gas (GHG) emissions in less than 30 years. In addition, the European Climate Law includes an intermediate target of 55% GHG emission reduction by 2030 compared to 1990 levels. The Fit-for-55 process has resulted in significant changes to Europe’s emission trading system (EU ETS) and raises the question of how to deal with residual process emissions in a net-zero world.

The European carbon market has since 2005 delivered significant emission reductions based on a robust regulatory framework. The EUA price has increased over the past years due to a significant tightening of the supply side and a focus shift towards industry-related abatement which is typically more costly compared to abatement in the power sector. The next regulatory focus shift needs to be towards removals to incentivize a net-zero-compatible market.

On the path to net-zero, the European Union Allowance (or EUA) is going to be on the red list of threatened species during the fifth trading period of the EU’s carbon market and is forecasted to be extinct by 2040. The revised EU ETS implements a significant tightening of the cap, hence the number of allowances distributed to the market is equivalent to the emissions allowed in the system.

The EU ETS cap before and after the legislative review – going to zero much earlier.

With this policy framework in place, net emissions in the EU ETS need to reach zero during 2039. The EU ETS towards “Day Zero” will differ from today’s market.

Two main challenges arise:

Availability of allowances. A continuously tightening cap results in decreasing availability of allowances to market participants who must comply with the EU ETS. The EU ETS has increasingly triggered interest from the financial sector as an investment vehicle towards a low-carbon future. In a market with a diminishing cap and increasing appetite for allowances, liquidity will reduce over time making it more difficult for compliance operators to get hold of allowances.

Need for negative emissions. Some emissions cannot be avoided entirely, mainly from industrial processes which can’t be reduced further due to technology boundaries. At the same time, the EU ETS cap effectively limits the number of new allowances in the market. This will inevitably square the circle in today’s regulatory world as these emissions need to be backed up by one allowance per ton of carbon while there won’t be any allowances left in the system. Hence the discussion about carbon removal credits is getting more and more prominent and with them the question of how to incentivize projects and ensure credibility and fungibility with the already existing carbon market framework.

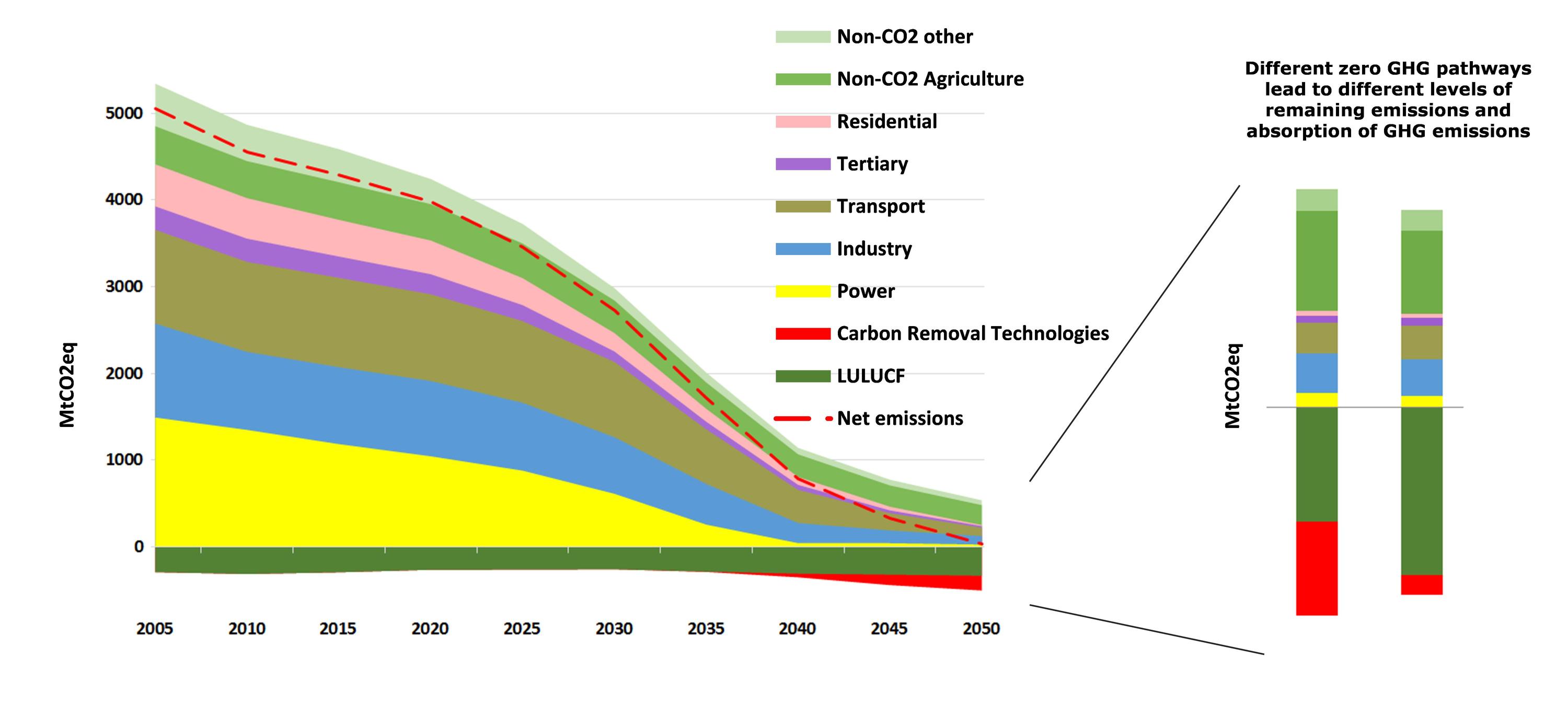

European Greenhouse Gas emissions trajectory in a 1.5 degrees scenario (European Commission)

There have been several suggestions recently to create a Carbon Central Bank to steer liquidity in the market as well as to pre-finance and incentivize removal credits towards 2040 and beyond.

The liquidity in the EU ETS will by nature reduce with a finite cap. That said, the scope extension of the ETS 1 (power sector and industry) over time by adding new sectors such as aviation (in 2012), various new sectors by the start of phase 3 in 2013 and the maritime sector (as of 2024) resulted in additional abatement options becoming available while the cap continuously covered a larger share of European emissions. The creation of a new ETS 2 including the fuel distribution for commercial road transport and buildings as of 2025 will create a sister system that at some point might converge to one large all-encompassing ETS, again potentially increasing liquidity in the system for a period.

It is important that especially at the point in time when the cap approaches zero, increasing liquidity is provided by carbon removal credits. Towards 2040 a matching number of removals floating the system is required to clear the market during any given year with residual industry emissions. This does not require a Central Bank approach with a central institution deciding on when to release a number of credits. It rather requires a functioning market that sets the right incentives towards creating such allowances.

The inflow of removals will lead to the morphing of a policy-steered market where the cap sets the supply maximum to a removal-based market where the amount of GHGs removed (and accredited in an EU ETS context) will set the supply maximum. The creation and flow of removal credits into the EU ETS will de facto set the price. It will probably also widen the scope towards the global aspects of carbon pricing, as removals might or might not be transferred via Article 6.4 of the Paris Agreement for accounting against residual emissions elsewhere on the globe. On a global scale, removal credits will likely be a sought-after commodity and it will largely depend on domestic regulatory frameworks as to how these credits can be exported.

The delivery of a significant quantity of removal credits requires investment into often very expensive technology to ramp up the ability to generate such credits at the scale required when “Day Zero” approaches. Advocates for a Central Carbon Bank argue that such an institution is required to ensure reliable advance financing of removal projects.

The genuine problem with a Central Carbon Bank approach, however, will always be the determination of the appropriate market conditions in terms of price offer or volume required to clear the market. Allowing pre-purchasing of carbon removals, described by one paper as a requirement to counterbalance future price risk is not much different in effect than a liquid forward market with physical delivery at contract expiry.

It is not the lack of foresight regarding future prices that is the issue but the lack of foresight regarding the regulatory framework and eligibility of removal credits within the EU ETS that causes the perceived problem. In case removal credits were to be allowed for compliance purposes in the EU ETS, a clear incentive was given to developers of such projects to go ahead and price these credits in an ETS context.

With a clear regulatory foresight as we have today with the Fit-for-55 legislation for the year 2030 and a net-zero indication in 2040, industry sectors should do everything possible to reduce emissions, also applying more costly abatement options while focusing on even more expensive removal credits to neutralize the residual emissions. To allow removal credits to be issued at a large scale, a regulatory framework is required to unlock the scale-up of the removal industry through the carbon price.

Negative emissions are not yet recognised in the existing EU ETS framework. That said, the removal debate is scheduled for the next EU ETS review considering a binding 2040 emission reduction target, which is scheduled to be done by June 2026. Given the urgency in getting the removal framework and incentive system up and running, this might already be very late. The European Commission has recently concluded a consultation as part of its preparation for the 2040 target-setting process, due to kick off with a formal target proposal in 2024. The assessment will provide insights into the required sectoral transformations over the coming decades resulting in deep emission reductions and increases in carbon removals.

A regulatory framework needs to be created for accepting carbon removal credits within the EU ETS. Though the EU ETS can provide a real demand center and economic incentive for scaling high-quality, engineered carbon removals, the policy design choices will have to walk a fine line to ensure that removals do not decrease the urgency of emissions reductions and that the removals that are included receive the same level of scrutiny as positive emissions in the scheme.

To maintain the objective of emission reductions, this can include conditions such as the location of the project (domestic/global), the difference in removal type and a certain “quota” to be allowed to enter the market – similar to what was the case for CDM and JI credits during trading phases 2 and 3 of the EU ETS. This time it will be for techniques such as nature-based removals, BECCS and DACCS. The allowed share of removal credits entering the market will need to be informed by the storage permanence of the methodology applied. The EU is developing a carbon removal certification framework as a first step to ensuring the environmental credibility of removal projects – and removal credits in the future.

In the end, the principle of “a ton is a ton” will have to be respected when discussing the permanence of removals. It needs to be guaranteed that the negative ton remains in the ground if matched with a positive ton towards an emission reduction target. Only then, the accounting adds up and only then, we can start debating a net negative emission pathway. To achieve this, a robust regulatory framework is required but not another institution, such as a Carbon Central Bank.

That said, even in case of a clearer regulatory picture, early investments into the rather expensive removal technology would still face the dilemma of requiring upfront financing.

Some of the removal technologies like DACCS will likely not receive enough pre-investment signals via todays and the forecasted carbon price. For such more costly technologies, marked-based incentives should at least initially be coupled with public funding where the ETS can also play an important role via member state auction revenues as well as the Innovation Fund.

Member states are required to use their auction revenues for climate- and energy-related purposes. On average, member states reported having spent 76% of auction revenues for such purposes in 2021. The Innovation Fund focuses on highly innovative technologies and flagship projects within Europe that can bring about significant emission reductions and is equipped with approximately 530 million EUAs following the latest legislative review.

As with all expensive technology, especially when looking into industry abatement solutions, the carbon price will not be the only incentive to put a project in motion but can in many cases help to build the business case for such an investment. That said, such funding will dry out over time given a shrinking cap and hence a decreasing number of allowances available for such funding despite an expected increase in carbon prices over time. The incentive system for removal projects should hence be launched now when there is still ample supply in the non-removal segment of the market to help a critical mass of the early movers jump over the fence.